Top equity funds that invest in small-cap stocks have tripled their NAV (net asset value) in the last three years. This has helped turn the category into an overnight sensation. Small-cap funds have raked in about ₹10,100 crore of the ₹17,900 crore that flowed into equity funds in the April-June 2023 quarter. In a recent Twitter interaction, a participant asked if he could move all his investments into small-cap funds, as the top fund had seen its NAV shoot up from about ₹9 ten years ago to ₹113 now.

A lot of the flows into small-cap funds today seem to be driven by the hope that their stellar run will continue. But going overboard on any fund category after it has had a great run is a cardinal retail mistake that often leads to grief. Making good returns on the small-cap category requires some strategising. Here’s how you can win with small-cap funds.

Know what’s normal

Compared to any other fund category, small-cap funds face big swings in returns. Looking at their performance for a particular five or 10-year period and expecting an encore can lead to disappointments.

Anyone looking at the trailing one1-year, five5-year and 10-year returns on small-cap funds today is bound to be blown away, because they average 28 per cent, 18 per cent and 22 per cent respectively. (All return references are to CAGR or compounded annual growth rate). In contrast, BSE Sensex has delivered 20 per cent for one year and 13 per cent for five5- and 10-years. But these returns are not a normal occurrence for small-cap funds.

Point-to-point return comparisons are always distorted by the start and end dates for the data. Today, 10-year returns on small-cap funds look phenomenal because July 2013 was a low point for Indian markets, with the BSE Sensex languishing at 19,000 levels and the BSE Smallcap 250 index at 900. From that point, the Sensex has tripled and the BSE Smallcap 250 has shot up fivefold. But there have been many 10ten-year periods when small-cap funds have earned lacklustre returns. For instance, in the ten years to July 2020, small-cap funds had made a mere 8 per cent CAGR.

Running a rolling return analysis (which looks at multiple point-to-point returns over a long time) is useful to gauge the returns that an average investor is likely to have made on small-cap funds. A rolling return analysis on monthly data for the BSE Smallcap250 index for the last 18 years (September 2005 to June 2023), shows that the average returns managed by this index over 5-year periods was at a modest 7.2 per cent and for 10-year periods at 7.8 per cent.

Poor averages for the Smallcap 250 index stem from the yawning gap between its best and worst periods. While this index has managed a staggering 23 per cent return in its best five5-year period, it lost 8 per cent annually in its worst five5-year spell. In its best 10-year period, it managed a 15 per cent CAGR (better than the Sensex’ 12 per cent), but in its worst decade it suffered a 1 per cent annual loss.

Thus, investors excited by the past five-year or 10-year returns on small-cap funds today, need to know that they are looking at one of the best periods on record for this category. Going by the law of averages, after delivering outsized returns in the last 10 years, returns on small-cap funds could very well revert to normal, or (god forbid) below-normal over the next 10 years. The ‘normal’ 10-year return on active small-cap funds has been 15-16 per cent. This should temper your long-term return expectation from this category.

As small-cap funds tend to swing between extremely good and terribly bad returns, the size of your small-cap investments and SIPs should not be out of proportion to your overall equity portfolio. Decide on a specific allocation to small-cap funds within your equity portfolio based on your risk appetite (say, 10-25 per cent) and size your lump sums or SIPs accordingly. Resist the temptation to load up on this category during good times.

Have a 10-year horizon

On a trailing return basis, small-cap funds have delivered great returns over the last one, three and five years. But the shorter your holding period in a small-cap fund, the higher is your chance of making losses from it or earning measly returns. The above rolling return analysis shows that for investors who held the small-cap index for one-year periods, it delivered a loss 41 per cent of the time. For those who stretched their holding period to five years, losses cropped up 17.5 per cent of the time. For those who held on for 10 years, losses were a minuscule possibility, occurring only 2 per cent of the time.

This offers two takeaways for investors. One, do not invest any money in small-cap funds that you are looking to pull out within 10 years. Over one-, three- or five-year time frames, the chance of exiting with sub-par returns is high. Two, given that markets seldom give advance warning of a correction or a bear phase, it is best for first-time investors to take only the SIP route to this category. This is also why most small-cap funds bar lump sums and gate SIPs in bull markets.

Invest after a fall

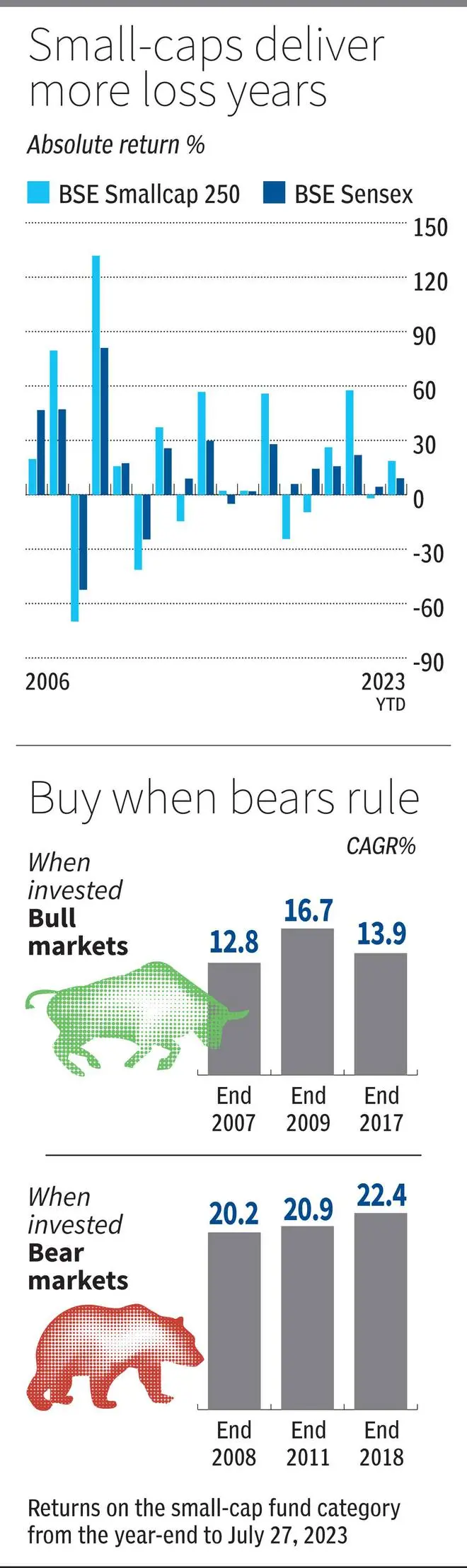

Small-cap funds subject their investors to a stomach-churning journey. The BSE Smallcap 250 index has had roughly double the number of loss-making years as the Sensex since 2006. Whenever the Sensex has sunk into a bear market, the Smallcap index has tumbled much harder. In 2008, the Smallcap index lost 69 per cent compared to the Sensex’ 52 per cent fall. In 2011, it fell over 41 per cent against 24 per cent on the Sensex. In 2018, small-caps lost 24 per cent while the Sensex gained.

When a fund you own loses 40 or 70 per cent of its value in a year, it can be very tough to hang on to it, and continue your SIPs. Yet, holding on is essential to enjoy the high long-term returns that follow bruising bear markets.

This is why roaring bull markets are bad times to make your first investments in small-cap funds. When the inevitable correction arrives, the tendency to panic and switch out, or stop SIPs, can be high. A good way to avoid the behavioural mistake of bailing out too soon is to start your small-cap fund investments after a big market fall. This can help you stay the course with your investments and vastly improve the long-term returns you get to make.

Our analysis (table 3) shows that had you invested in small-cap funds after big bull years such as 2007, 2009 or 2017, your average returns till date would have ranged at 12.8-16.7 per cent. But had you invested after big market falls in 2008, 2011 or 2018, you would have easily managed a 20 per cent return.

Gauging market tops or bottoms is possible only with the benefit of hindsight. But to enjoy better returns from your small-cap funds it is enough to invest after a significant market (Sensex) fall (say, 20 or 30 per cent). First-time investors with no small-cap allocation can start out with small SIPs in bull market and add to them on significant declines. Seasoned investors with an existing small-cap allocation can stay off adding to it in bull markets and bide their time on additions (SIPs or lump sums) until the market falls.

Active over passive

In the large-cap and mid-cap categories, active fund managers have been finding it difficult to beat their benchmarks in recent years. This has led to investors shifting to passive funds tracking indices such as the Nifty50, Nifty100, Nifty Midcap 150 and Sensex30. While some investors own passive-only portfolios, others mix and match active with passive funds.

The small-cap category has also seen the launch of many index funds in the last couple of years. The menu now includes index funds tracking the Nifty Smallcap 50, Nifty Smallcap 250 and the Nifty Microcap 250 indices. So, should you take the passive route to small-cap funds too?

The active fund route to small-cap investing seems to score over the passive route for three reasons. One, on an average, active small-cap funds have still managed to beat their benchmark (BSE Smallcap 250 index) over three-, five- and 10-year time frames. While the index managed returns of 39.1 per cent, 15.1 per cent and 18.1 per cent over these time periods, active small-cap funds averaged 39.2 per cent, 18.1 per cent and 22.4 per cent respectively. The margins by which the top funds beat the indices is 4-5 percentage points.

Two, unlike the large-cap or mid-cap spaces where active managers have a limited universe of stocks to choose from (100 large-caps and 150 mid-caps by the SEBI definition), the small-cap category opens up a large playing field for active stock selection (all stocks beyond the top 250). After SEBI’s categorisation norms in 2018, the market cap cut-off for the small-cap segment has moved up from ₹5,000 crore to ₹17,000 crore.

Three, careful stock selection is critical to win at small-cap investing in the long run and this is better achieved with active funds. Small-cap investing in India, unlike large-cap or mid-cap investing, is prone to high governance as well as business risks. About a third of the small-cap stocks that were listed 10 years ago aren’t even traded today. Most small companies fail to scale up to a meaningful size. Given the many qualitative factors that go into identifying small-cap survivors, this is a space for fundamental investing. As index providers select their small-cap index constituents based mainly on market cap and liquidity and not governance, valuations or fundamentals, active managers can build a better-quality portfolio of small-cap stocks than the index providers.

Choosing active small-cap funds

Hitherto, we’ve discussed how investors should time their bets on small-cap funds and recommended the active route. But given the wide gaps in returns between the leader and laggard funds within small-caps, how can investors choose the right active funds? We suggest the following filters.

- In the small-cap space, bull markets make every investor (and fund manager) look like a genius. To ensure that your small-cap fund’s returns are the result of some skill, and not plain fluke, look for funds that have existed over entire market cycle (a bull and bear phase). They should have fared better than the index in both. Given that the last big falls in the small-cap space transpired in 2011 and 2018, look for funds that have been around since 2010. Go for a fund with a long track record even if it has a large asset size.

- Selecting small-cap stocks in India is a very different ballgame from choosing mega or mid-caps. Small-caps require a bottom-up approach with an ear to the ground on governance and management moves. Look for small-cap funds with a specialist manager — who isn’t juggling a battery of large- and mid-cap funds in the same fund house.

- In India, the small-cap space is a value investing minefield. Small-caps that trade cheap are often those bogged down by governance or business risks. Gravitate towards small-cap funds managed in the growth or quality styles, rather than value-style ones. Don’t shy away from funds with a high portfolio PE as this may be an indication of better business quality.

- To manage inflows and risks, small-cap fund managers have leeway to invest upto 35 per cent of their corpus in cash equivalents, large-cap or mid-cap stocks. Check how a small-cap fund is using this leeway. Cash calls in frothy markets may allow a fund to manage downside better than peers. Allocating more to mid-caps rather than large-caps can give a return kicker. Based on the above factors, Nippon India Smallcap and SBI Smallcap funds can be considered.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.